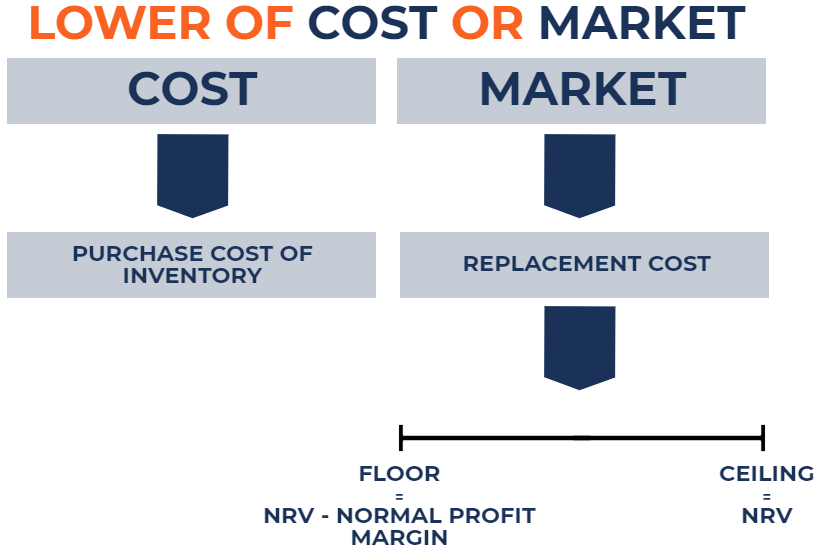

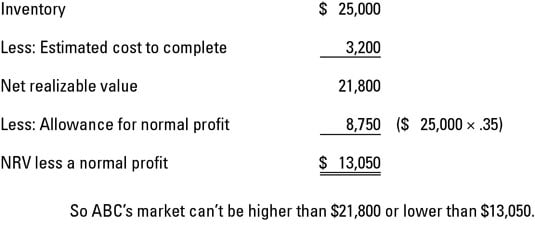

The Floor To Be Used In Applying The Lower Of Cost Or Market Method

Lower Of Cost Or Market Value Rule Lcm Accounting Explained Market Value Marketing Cost

Lower Of Cost Or Market Lcm Definition Inventory Valuation Examples

How To Use Lower Of Cost Or Market Dummies

Lower Of Cost Or Market Rule For Valuing Inventory Youtube

Class 5 Lower Cost Or Market Ppt Download

Lower Of Cost Or Market Lcm Accounting Rule Examples Explained

The floor to be used in applying the lower of cost or market method to inventory is determined as the a.

The floor to be used in applying the lower of cost or market method.

Lower Of Cost And Net Realizable Value Lcnrv Open Textbooks For Hong Kong

How To Innovate To Address The 4c Challenge For Rail Innovation Challenges Parker Hannifin

Price Controls Price Floors And Ceilings Illustrated

Lower Of Cost Or Market Rule Example Youtube

Source : pinterest.com